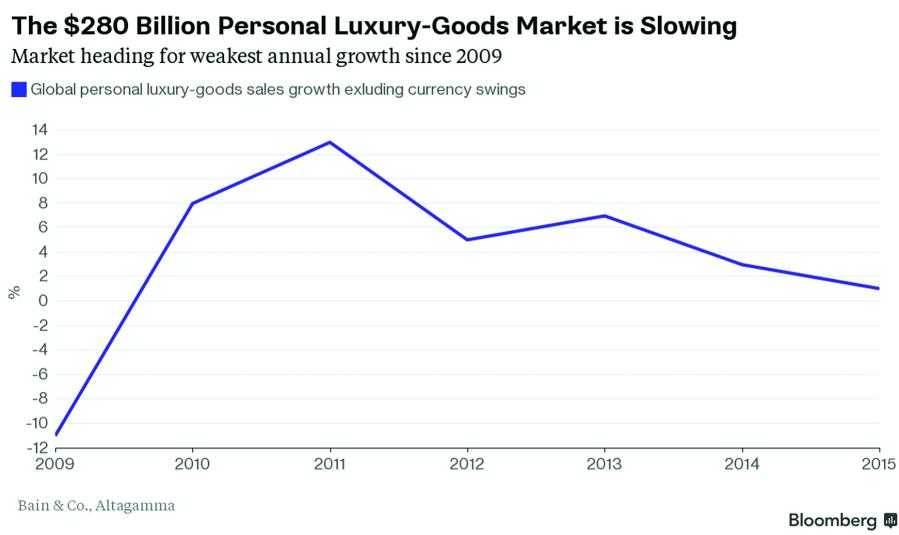

After enjoying over five years of continuous growth, the turmoil in the stock markets, combined with a strong dollar and a commodity-price disorder curbing demand, is resulting in the global personal luxury goods market to head towards the weakest year since the Lehman crash, according to the recently released report on luxury market by Bain & Company, a management consultancy.

As tracked by Bain & Co., the sale of items such as designer dresses and shoes will rise as little as 1 per cent to US $ 280 billion in 2015, which in May forecasted a growth of 2 to 4 per cent. “It is getting harder to compete. In a best-case scenario, the market will expand 2 per cent assuming strong demand over a holiday period. The challenge for luxury brands in this environment is how to successfully navigate through hard-to-predict volatility,” informs Claudia D’Arpizio, Partner, Bain & Co. This would be the weakest gain since sales fell 11 per cent in the year after Lehman Brothers’ collapse, a projection that is on a basis that excludes currency swings.

Such is the current situation that luxury labels such as Louis Vuitton and Burberry are facing difficulty even in China, which was the fastest growing luxury market in the past few years as the slowing economy is worsening the effect of the Government’s antiextravagance drive, eating into the demand for handbags and coats. LVMH was the first major luxury goods provider to say that the stock market collapse in China over the summer had affected sales, particularly at its flagship store Louis Vuitton. According to Bain & Co., “US growth has softened due to the stock market volatility and a strong dollar curbing purchases by locals and tourists. The luxury goods sales will fall for the second straight year in China, while the segment in the US won’t grow.”

Ironically, while the US currency is getting stronger and is affecting sales, the weaker Euro is somehow helping the luxury market to gain amidst volatile situations. Bain & Co. has estimated that the currency movements will boost the value of luxury sales by ¤ 26 billion (US $ 27.73 billion) this year, as Chinese consumers are shopping in places with weaker currencies boosting their pricing power, particularly in Japan and Europe. “The Chinese shoppers will account for almost a-third of global luxury spending, up from 28 per cent in 2014,” forecasts Bain & Co.

An analysis of European taxfree shopping data, conducted in partnership with Global Blue, shows that Chinese tax-free purchases have increased by 64 per cent, particularly among the accessible and aspirational luxury segments due to the weakening of Euro. Also, Americans have increased their tax-free spending in Europe by 67 per cent, aiming largely at the high end of the luxury spectrum. But, Russians have cut down there European spending by 37 per cent, and spending amongst the Japanese in Europe has also withered by 16 per cent.

Get Access to more Retail Destination articles from APPARELRESOURCES.COM. SUBSCRIBE TODAY

“Undoubtedly, Chinese consumers play a primary role in the growth of luxury spending worldwide. For years, we have known that they spend far more abroad than in Mainland China, but what’s changing is that they’re spending little money in historically popular destinations, such as Hong Kong and Macau, and are instead gravitating to new locales, such as Europe, South Korea or Japan, to benefit from currency fluctuations that drive favourable price gaps,” reveals Federica Levato, co-author of the Bain & Co. study.

In regard to the exchange rates, the US market did not deliver this year due to the dollar being expensive for many global tourists, though local consumption grew but it was not sufficient to offset the loss in tourism revenue. Despite this, the US is the largest luxury market in terms of global luxury value, reaching ¤ 79 billion (US $ 85 billion); New York City alone outweighed all of Japan. Even so, Japan has proven to be a consistent champion, driven by a sound base of local consumers and the emergence of Chinese shoppers looking to capitalize on currency fluctuations.

While, Asia has registered the worst historical performance due to the lacklustre trends in Mainland China, in combination with the sharp drop in sales in Hong Kong and Macau. The personal luxury goods market in Hong Kong and Macau has fallen victim to a number of Government measures aimed at regulating the grey market in China, creating a 25 per cent contraction in real terms. Though local spending in China continued to decrease but the appreciation of the local currency has boosted the country to No. 3 spot in terms of global luxury value, overtaking Italy and France, trailing only by the US and Japan, as per the Bain & Co. report.

However, this growth is expected to strengthen in the coming year that too in the latter part. As Claudia points, “The luxury market growth is to strengthen from the second quarter of 2016. This ‘new normal’ for the luxury market is growth of 3 to 4 per cent.” The personal luxury goods market, including leather accessories, fashion, hard luxury and fragrance & cosmetics has reached ¤ 253 billion (US $ 270 billion) in 2015, representing 13 per cent growth at current exchange rates. Though 2015 seems to be heading towards being the weakest year since 2009, but luxury brands are leaving no stone unturned in captivating the attention of price-conscious buyers by strategizing such as going online, which is quite new for a majority of luxury brands. It is steps as these, which will propel the luxury market, though its fate still seems to be restricted in terms of growth for 2015.

Post a Comment