India has been a prominent sourcing hub for a variety of goods and textile is one of the dominant categories for which India is always looked upon by the global buyers. Despite a slump in its apparel exports in recent year, India is still considered a preferred destination for apparel sourcing, because of the fact that the country can adapt to the ever-evolving fashion trends and make smoother transition in its production units – thanks to its upper-hand in producing high-fashion garments.

The speculations of increased sourcing from India aren’t hyped for no reason. While India’s neighbouring competitors in apparel manufacturing still struggle to cater to smaller quantities – something that’s become a new-norm amidst compressed consumers’ spending – the added advantage to the Indian manufacturers is that the growing domestic apparel retail market (worth US $ 80 billion) has emerged as the saviour of the manufacturing industry. Adding to this are the efforts of apparel factories that are organising an aggressive vaccination campaign to achieve the inoculation of their workforce in order to see factories running in full operation. This also puts India ahead of its competitors in long-run as the buyers can rely on the world’s largest vaccination drive which is sure to bring business activities on track without any major ruckus or stoppage in coming months.

Apart from this, what makes to the list is the talk between India and EU as both have agreed to restart the long-halted free trade agreement (FTA) in an effort to strengthen their economic cooperation especially amidst the fast growing influence of China. There’s no better way for Indian garment manufacturers to closely compete with Bangladesh and Vietnam, which currently are getting preferential access, and this is going to boost EU’s sourcing from India.

Various reports and surveys conducted in 2021’s first 6 months also back the projected disruptions in supply side of the industry! QIMA – a leading provider of supply chain compliance solutions – conducted a survey in March ’21 that clearly indicated the continuing ‘regionalisation’ of global supply chains, with India as well as Vietnam coming into their own as China’s regional competitors. Both the countries are among key overseas sourcing markets for various industries including fashion sector, especially for USA and EU.

Current Outlook of Apparel Sourcing and QIMA Survey

The apparel supply chains are rattled by COVID-19; they were already undergoing severe transitions long before pandemic came into existence. The challenges imposed by global pandemic on apparel businesses are double-edged – 1) it’s very difficult to predict a time when and how quickly the consumption of clothing and related products will rebound amidst the resurgence of COVID cases worldwide; and 2) the buyer-driven apparel business will surely see disruptions in its sourcing habits and more companies will find alternatives of the conventional countries/regions such as China that has been the undisputed leading sourcing destination for years.

This is important to understand that the brands and companies are avoiding their ‘complete reliance’ on China while keeping it at the centre of the sourcing strategies as well as identifying vulnerabilities to material shortages and having contingency plans.

QIMA survey says that 71 per cent of the global respondents from textile and apparel sector are planning/considering a switch to suppliers in new regions in the coming 12 months! 43 per cent respondents named Vietnam among their TOP 3 (vs. 36 per cent in 2020), while the share of USA brands naming India as a TOP 3 sourcing market doubled in H1 2021 vs. H1 2020. Meanwhile, the diversification away from China continues, albeit at a slower pace. The share of respondents globally naming China among their TOP 3 sourcing geographies in H1 2021 remained virtually unchanged (for all industries) at 74 per cent vs. 75 per cent on Y-o-Y basis, but the sourcing of apparel products is seeing a continuous decline in China.

Sourcing from India back in the spotlight

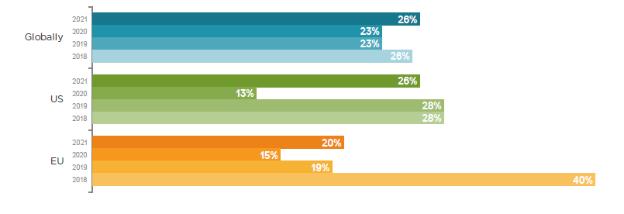

After a temporary dip in popularity during 2020, India has returned to the forefront as a sourcing destination and named among the TOP 3 sourcing partners by over one quarter of respondents globally, as well as in the USA – as per QIMA survey. (See Image 1)

Image 1: Percentage of respondents naming India among their TOP3 sourcing partners – by HQ location (Source: QIMA)

Among those respondents who pursued geographical diversification of sourcing last year, 28 per cent globally (and 32 per cent in the USA) opted for suppliers based in India in 2020 – and as many are reporting plans to buy more from India in 2021. However, the report indicates that, no longer pigeonholed as a textile hub, India is a prominent sourcing choice for a variety of consumer goods such as fashion accessories (33 per cent) and footwear (32 per cent).

Another leading data and analytics company GlobalData recently released a report and stated that the time is ripe to expand sourcing from India and Vietnam as restrictions start to come into force in major markets on fabrics and other products sourced from China.

Respondent expectations for China sourcing in 2021

The relationship of global supply chains with China has gone through multiple twists and turns in the past years, 2020 was no exception, and an impact is being clearly seen in 2021 as well. Already shaken by the fallout of the US-China trade war, the popularity of China as a sourcing market among Western buyers took another hit in early 2020.

Between 2020 and 2021, the drop in China’s global popularity has slowed to a crawl. Only 6 per cent and 11 per cent of US- and EU-based brands, respectively, would say that they did ‘significantly more’ sourcing from China in 2020. When the data is translated to apparel and textile industry, the condition of China is not satisfactory. Only 6 per cent global respondents said they increased apparel/textile sourcing ‘significantly’ from China in 2020; 12 per cent stated ‘no change’ in their China sourcing; 29 per cent asserted their China sourcing ‘decreased somewhat’; while 15 per cent claimed they reduced dependency on China ‘significantly’.

After witnessing a dent in reputation, China’s 2021 outlook seems a mixed bag of sourcing expectations of respondents. 40 per cent respondents have planned to buy as much or even more from Chinese apparel suppliers; 25 per cent have plans to buy less from Chinese suppliers as well as move their facilities from China; and 19.50 per cent said they will buy less from Chinese suppliers, but don’t have plans to move facilities from the country.

Why these disruptions?

There are multiple factors behind such disruptions in the global apparel sourcing chain. As Apparel Resources keeps a close eye on these disruptions, our team has covered a lot articles recently telling our readers how sourcing is being impacted and why India is looked as a preferred supplier! Here are some of those articles –

The buying sourcing trends as the pandemic takes a full circle back to Asia

The changing sourcing tides of the post-pandemic market

Will brands consider responsible sourcing in the post-pandemic world?

What lies ahead?

While the seismic disruptions of the pandemic are likely to continue affecting the world in the months to come, there is room for optimism in the global sourcing outlook of 2021. The pandemic has shown that for any business involved in sourcing, true resilience requires agile, flexible, well-connected supply chains – and the trends observed among the respondents of QIMA survey suggest that businesses are taking this valuable lesson to heart. As global trade continues to emerge from crisis mode, more companies are expected to put these insights into practice and increasingly embrace diversification and flexibility as long-term strategies for future-proofing their sourcing.

Post a Comment